We Think Corvus Pharmaceuticals (NASDAQ:CRVS) Needs To Drive Business Growth Carefully

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Corvus Pharmaceuticals (NASDAQ:CRVS) shareholders is whether they should be concerned by its rate of cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Corvus Pharmaceuticals

How Long Is Corvus Pharmaceuticals' Cash Runway?

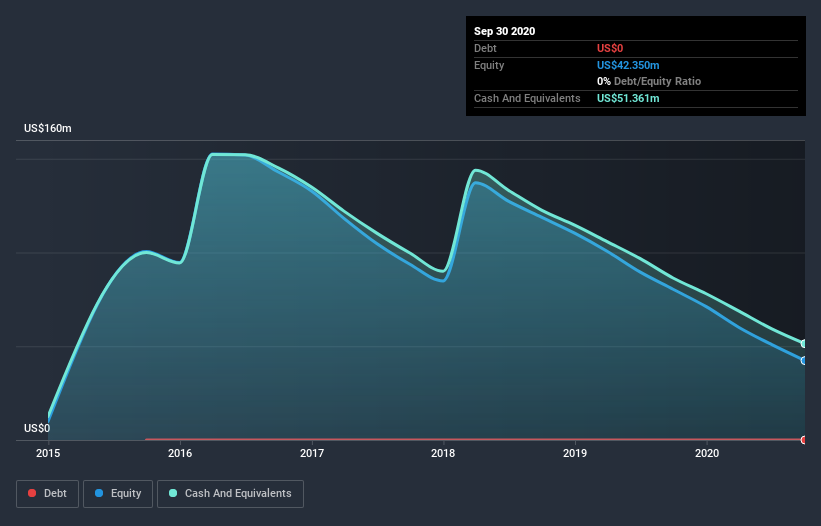

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When Corvus Pharmaceuticals last reported its balance sheet in September 2020, it had zero debt and cash worth US$51m. Importantly, its cash burn was US$35m over the trailing twelve months. So it had a cash runway of approximately 18 months from September 2020. While that cash runway isn't too concerning, sensible holders would be peering into the distance, and considering what happens if the company runs out of cash. Depicted below, you can see how its cash holdings have changed over time.

How Is Corvus Pharmaceuticals' Cash Burn Changing Over Time?

Corvus Pharmaceuticals didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. With cash burn dropping by 5.5% it seems management feel the company is spending enough to advance its business plans at an appropriate pace. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Easily Can Corvus Pharmaceuticals Raise Cash?

While Corvus Pharmaceuticals is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Corvus Pharmaceuticals' cash burn of US$35m is about 32% of its US$111m market capitalisation. That's not insignificant, and if the company had to sell enough shares to fund another year's growth at the current share price, you'd likely witness fairly costly dilution.

Is Corvus Pharmaceuticals' Cash Burn A Worry?

Even though its cash burn relative to its market cap makes us a little nervous, we are compelled to mention that we thought Corvus Pharmaceuticals' cash runway was relatively promising. We don't think its cash burn is particularly problematic, but after considering the range of factors in this article, we do think shareholders should be monitoring how it changes over time. On another note, we conducted an in-depth investigation of the company, and identified 2 warning signs for Corvus Pharmaceuticals (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

Of course Corvus Pharmaceuticals may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.